Is Super Micro Computer Stock Headed for $15 or $70 After Giant Post-Earnings Plunge?

/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)

After putting accounting controversies and Nasdaq delisting fears stemming from the delayed filings in the rearview mirror, Super Micro Computer (SMCI) had been on a strong recovery run this year. SMCI stock once again regained traction as investors bet big on its leadership in the artificial intelligence (AI) hardware space, growing demand for next-gen servers, and close partnership with chip giant Nvidia (NVDA) — all of which painted a promising growth story.

But the narrative took a sharp turn in the wrong direction after the company dropped its fourth-quarter earnings report on Aug. 5. Shares of SMCI sank more than 18% in the following trading session, as Super Micro missed Wall Street’s expectations on both revenue and earnings. Even guidance fell short, sparking fresh concerns about slowing growth and rising competition.

Investor sentiment around SMCI stock has clearly taken a hit, and analysts' opinions are now deeply divided. On one end, the most bullish target on Wall Street suggests that SMCI stock could soar to $70, while on the other side, the most bearish sees it dropping all the way to $15 per share. So, with expectations stretched so far apart, can SMCI defy the doubts and reclaim its momentum? Or is there more downside still to come?

About Super Micro Stock

Super Micro Computer specializes in building high-powered, energy-efficient servers to support surging demand from AI, cloud services, and data centers. With operations across the U.S., Taiwan, and the Netherlands, the company has built a solid international footprint and currently holds a market capitalization of $27.8 billion.

After sliding last year under the weight of negative headlines, SMCI stock came roaring back in 2025, hitting a fresh high of $66.44 in February. Even after pulling back some 32% from that peak, the stock remains up an impressive 50% so far this year, well ahead of the broader S&P 500 Index's ($SPX) modest 8.5% gain year-to-date (YTD).

However, the comeback rally appears to be facing turbulence lately. SMCI is once again under pressure following its latest earnings miss, with shares tumbling 19% in just the past five trading days.

A Look Inside Super Micro’s Q4 Earnings

Super Micro’s fiscal 2025 fourth-quarter earnings report released earlier this month came as a letdown to investors, missing Wall Street’s expectations on both the top and bottom lines. Revenue for the quarter rose 7.4% year-over-year (YOY) to $5.8 billion but still fell short of the $5.9 billion analysts had expected. Adjusted EPS came in at $0.41, marking a notable 24% decline from the prior year and falling below the consensus estimate of $0.44, partly because of the impact from President Donald Trump’s tariffs on goods imported into the United States.

While the company pointed to tariffs as a key reason for the earnings shortfall, the miss stung even more given the backdrop of soaring demand for AI infrastructure, which had set investors’ expectations sky high. Instead of a blowout quarter, the results revealed mounting cost pressures and thinner margins, casting doubt on Super Micro’s ability to deliver strong profits even as sales continue to rise.

A key red flag was the drop in gross margin, which slipped to 9.5% from 10.2% a year ago. The decline suggests the company may be facing pricing pressure or higher costs, likely tied to competitive dynamics or more expensive AI components. As of June 30, Super Micro reported $5.2 billion in cash and equivalents, alongside $4.8 billion in total bank debt and convertible notes.

Unfortunately, the disappointment didn’t end at Super Micro’s Q4 financials. The company’s guidance for Q1 of fiscal 2026 also fell short of expectations. Management expects revenue to land between $6 billion and $7 billion, while adjusted EPS is expected to be between $0.40 and $0.52. Both of these figures miss Wall Street’s forecasts for $6.6 billion in revenue and $0.59 in EPS.

Over the longer term, analysts tracking Super Micro project the company's bottom line to rise 19.2% YOY to $2.05 per share in fiscal 2026, then leap 21% annually to $2.49 in fiscal 2027.

What Do Analysts Think About Super Micro Stock?

After the disappointing Q4 showing, several Wall Street analysts struck a more cautious tone. For instance, JPMorgan analyst Samik Chatterjee lowered the firm’s price target to $45 from $46, maintaining a “Neutral” rating. Chatterjee pointed to capital constraints and customer hesitation as key reasons the company fell short of expectations.

On the other hand, Bank of America Securities analyst Ruplu Bhattacharya slightly raised the price target to $37 from $35 while sticking with an “Underperform” rating. The analyst noted that gross margins were pressured once again, this time due to inventory reserves for older products. Bhattacharya explained that many customers are opting to wait for Nvidia’s upcoming B300/GB300 GPUs, which has weighed on current demand.

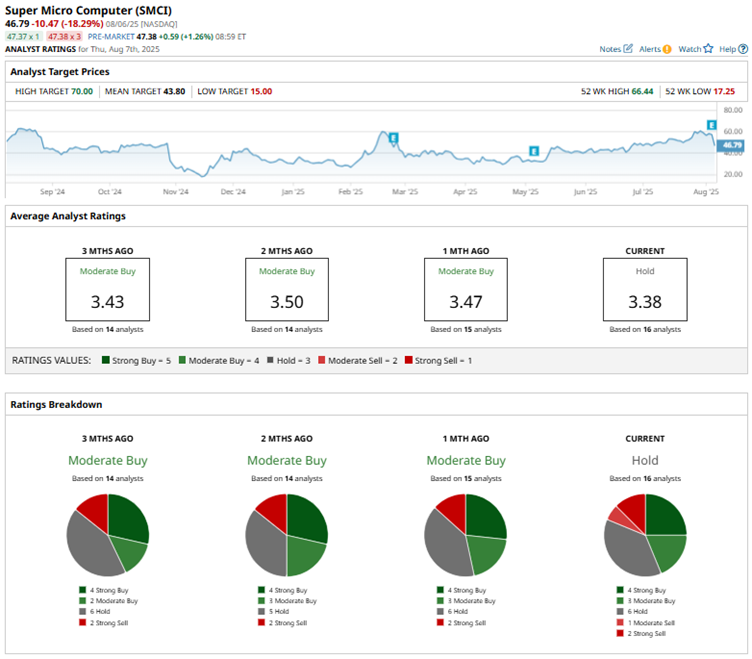

Overall, Wall Street sentiment on Super Micro is tilting cautious, with SMCI stock earning a consensus rating of “Hold.” Among the 16 analysts covering the stock, opinions are clearly mixed. Only four recommend a “Strong Buy,” while three lean toward a “Moderate Buy.” The majority of analysts take a wait-and-see approach, with six suggesting “Hold.” On the bearish side, one analyst has a “Moderate Sell” rating for SMCI and two assign a “Strong Sell” rating, reflecting growing uncertainty around the company’s near-term outlook.

SMCI stock has a Street-high price target of $70, indicating nearly 54% potential upside. The lowest target of $15 suggests a steep 67% drop from current levels.

Key Takeaways

Super Micro’s wide price target range, spanning from $15 to a Street-high of $70, underscores the uncertainty surrounding its near-term trajectory. While some analysts remain bullish on its long-term AI-driven potential, others are wary of execution risks and margin pressures. With sentiment this divided, the stock’s path forward may remain volatile as investors wait for more apparent signs of sustained growth.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.